A matter of less accommodation, not tightening

Market Flash

ECB to revise growth and inflation downwardly

End of APP is no monetary tightening but less accomodation

Subtle tweaks rather than major surprises

The ‘best’ market reaction is no market reaction

Same chorus, different meeting

Not much was expected from the latest ECB policy meetings. Indeed, the past few months in general held no significant modifications to either the monetary policy stance or the tone struck by Draghi in the press conferences following the ECB decision. The October meeting proved to be the most interesting however, given the bout of volatility that spread across all markets since the month’s start. The ECB President had to walk a thin line in acknowledging the market nervousness against a backdrop of increased economic uncertainty while in doing so not rattling frantic investors even further by suggesting the ECB shares their concerns to a material extent. The lack of a significant market reaction during the press conference suggests he did so masterfully.

The turmoil in equity markets, vulnerabilities in emerging economies, increased protectionism, Italy on an outright collision course with the European Commission and the brexit stalemate contributed to the downside risks to the Euro area economy. It is in such a context Draghi strongly defended the ECB’s previous (September) rather optimistic economic and monetary assessment. He delivered a similar view at the end of November, in one of his last public appearances to the European Parliament before the ECB’s blackout period.

Draghi mentioned that the data were “somewhat weaker than expected” lately, (implicitly) referring to, amongst others, continuously declining PMI confidence indicators and to the poor GDP growth of 0.2% QoQ in the third quarter. But in the President’s view, such a gradual slowdown is normal as expansions mature and growth eventually converges back toward potential. The poor Q3 growth performance has also to a great extent to do with country and sector-specific factors that are considered temporary. Draghi points out the car industry has been disrupted by regulatory issues in Q3 and already sees signs of normalization.

Meanwhile, the underlying drivers of domestic demand remain firmly in place. Household income is supported by ongoing labour market strength. Business investment in turn is facilitated by very favourable financing conditions.

On price developments the ECB chair’s confidence remains unabated. Headline inflation is boosted by energy base effects but underlying price pressures continue to be muted. Yet, Draghi sees good reasons for underlying inflation to gradually rise in the months ahead as wages are increasing and producer and import prices are recovering. Therefore the ECB remains convinced of a sustained convergence of inflation toward target, even after winding down the net asset purchases this month.

Subtle balancing act

Turning to the December meeting, we expect subtle tweaks rather than major surprises. The ECB wants to strike a delicate balance of reassuring markets while taking into account the increased risks surrounding the economic environment. Therefore, we expect Draghi to stick to the very gradually normalizing monetary policy path set out in June. In particular, we anticipate the ECB to keep rates at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

We see little reason for an extension of the net asset purchases, despite weaker than expected data. The ECB will bury the net asset purchasing programme by the end of December, also as plotted out in June. With regards to the reinvestment policy, we anticipate that the Governing Council intends to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

At the October meeting Draghi indicated multiple times that the assessment described above would be reviewed in the light of new economic projections. It will be particularly interesting to see whether and how the latest data and economic and financial developments have affected the ECB’s December forecasts. Given the softer activity data and increased uncertaintity, we anticipate a minor downward revision of growth for the current year while 2019 and 2020 projections remain unchanged. The ECB will also provide 2021 data, which we expect to show growth slowing but remaining solid. Inflation projections will also face a downward – oil price inspired – revision, reaching the ECB’s below but close to 2% target by the end of the forecasting horizon (i.e. 2021).

With these minor adjustments the ECB wants to signal the world economy is doing just fine but that it takes the risks into account. It will be key for markets to see whether the ECB sees these risks important enough to tilt the balance of risks, now broadly balanced, to the downside. Such a move would add to current investor worries and most likely aggravate market turmoil. Draghi will stress the current outlook warrants the (baby step toward) policy normalization but that given the reinvestment policy of the sizeable stock, it should be viewed as a less accommodative stance rather than a tightening move. This balancing act of being perceived not too hawkish nor dovish will be the thread running through the press conference.

Draghi triggered market attention at the last meeting by suggesting the ECB could, in theory, launch new long term refinancing operations ((T)LTRO’s) should the economic environment worsen dramatically. Given the recent data weakness, we expect a considerable amount of related questions. The central bank will probably reiterate the “richness” of its policy toolkit on Thursday while stressing there is no need of using it from a growth perspective, but he might nevertheless signal a roll-over in the run-up to large June 2020 maturity dates.

The ECB-President is also facing questions about Italy. As usual, Draghi will refrain of any high profile comments as it is a fiscal and no monetary matter. Furthermore, negotiations are still ongoing and the ECB is likely to await the conclusions on the matter drawn by the European Council that takes place the same day and the next. Regarding Brexit, Draghi will bring to mind the ECB’s collaboration with the Bank of England to ensure a smooth financial system following any type of Brexit.

ECB to brace for a credibility test

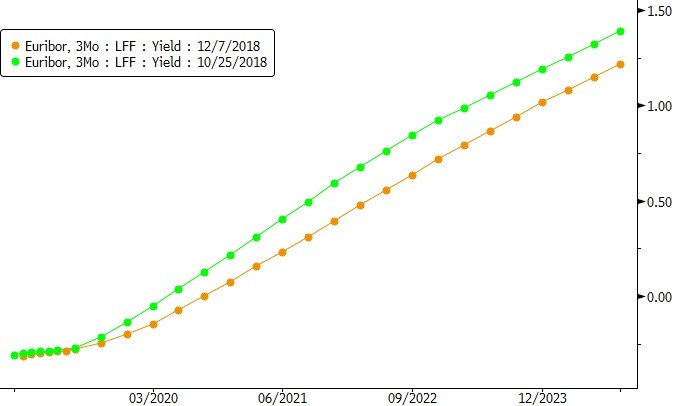

Against the backdrop of increased uncertainty and volatility, market expectiations turned very dovish ahead of this ECB meeting, questioning the normalization path set out in June. 3M Euribor rates aren’t expected to turn positive before the third quarter in 2020. EMU swap rates and German yields are at May 2018 lows. EUR/USD is trading sideways in a rather low 1.12/15 range. The end of the APP is largely discounted since its announcement in June and is, as such, unlikely to trigger a lasting market reaction. We don’t think the ECB’s intentions are to push for even lower market expectations. At the same time it will be key not to trigger any unwarranted financial tightening. We think Draghi’s verbal acrobatics during the Q&A will prove crucial for the matter. In this context, the lack of signifcant market moves should (again) be considered a success for the central bank. Here’s where the Fed meeting next week might come to aid. The US central bank is facing even more investor scrutiny after the heavy market repositioning of late. It’s very well possible investors stay sidelined until December 19.

Figuur - Markets only expect positive 3M Euribor rates in Q3 2020. Dovsih shift compared with October meeting (green).