Red wave on the US horizon as economic concerns rise

As the US is experiencing high inflation and declining consumer sentiment, talk of a red wave in this year’s November midterms is mounting. Yet surprisingly, Democrats still have a fighting chance, thanks to redistricting (which affects the House of Representatives) and a favourable composition of the Senate seats up for election this year. The outcome of this election will have major consequences. A Republican win will doom Joe Biden’s legislative agenda and increase the risk of prolonged government shutdowns. A Democratic win on the other hand, might lead to increased spending on climate change and social care among other policy initiatives. This US election will likely be determined by economic developments and will add even more uncertainty to an already uncertain world.

The US midterms are typically a referendum on the ruling president, often translating into a significant loss for the party in power. Historically, the party controlling the White House has lost an average of 28 House seats in midterm elections. Democrats currently only hold a 12-seat advantage over Republicans in the House of Representatives (with 3 vacancies previously held by Republicans) and a 1-vote advantage in the Senate. So, thin margins separate the Republican party from regaining control over either or both chambers of Congress. Furthermore, President Biden’s net approval rating of -11% bodes ill for the Democratic Party.

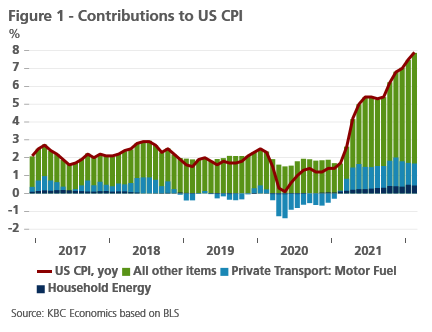

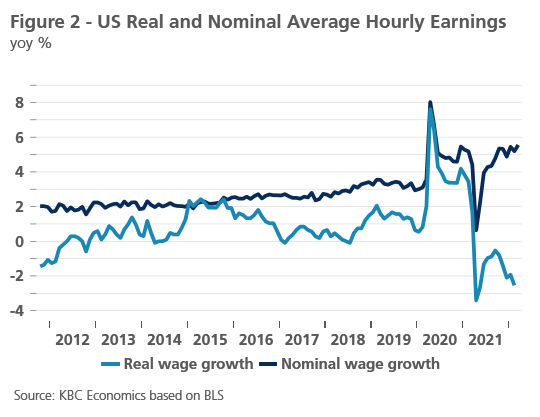

Economic developments, and particularly the state of the labour market, normally play an important role in the president’s approval rating. However, with an average of 564,000 net jobs added every month since Biden took office, the unemployment rate back down to 3.8%, and total unemployment only about 1 million jobs off from the pre-pandemic peak, there are clearly other factors currently dragging down Biden’s popularity. One such factor is the quickly rising inflation rate, with headline CPI hitting 7.9% yoy in February. While core inflation has also trended higher, higher energy costs have been a major driver, accounting for about one-fifth of the latest inflation figure (figure 1). While the contribution from motor fuel has eased slightly since November, the latest spike in oil prices, and therefore gasoline prices, as a result of the war in Ukraine will only drive inflation higher in the coming months. Indeed, higher inflation is clearly offsetting gains in wage growth stemming from the tight labour market, with real hourly earnings contracting on a year-over-year basis for the past eleven months (figure 2).

It is worth noting that geopolitical factors have also contributed to Biden’s low approval rating, with his net popularity dipping into negative territory right around the US withdrawal from Afghanistan and staying there ever since. The war in Ukraine doesn’t seem to be moving the needle much for now. While 58% of Americans believe the current administration has done a good job of avoiding direct military conflict with Russia, only 36% rate Biden’s overall response as good.

Is a red wave coming?

Despite these negative omens, Democrats still have a reasonable chance of keeping their majorities in both chambers. Current polls give Republicans a mere 2.3 ppt advantage over Democrats, a far cry from the 8.6 ppt margin of victory of Democrats in 2018 or the 5.7 ppt margin Republicans had in 2014. A 2-3 ppt swing in favour of the Democratic Party would be well within the margin of error and could happen if, e.g., inflationary pressures ease and/or turn out for the Democrats is high.

The current redistricting cycle also improves Democrats’ chances in the House. At the beginning of every decade, states (often state legislatures) redraw electoral districts using new census data, and often try to gain a partisan advantage (a tactic called gerrymandering). In the 2010 redistricting cycle, Republicans gained the upper hand, but the 2020 redistricting cycle has so far been more favourable to Democrats (though the process isn’t over yet).

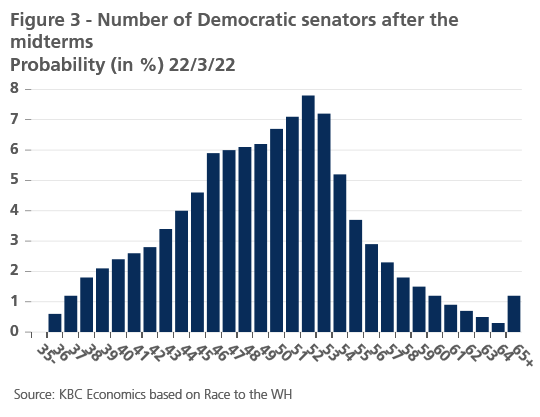

The Senate map is also relatively favourable to Democrats in this midterm election (figure 3). In the House, all members are up for re-election, but in the Senate, only a third of senators are elected every election cycle. The 34 Senate seats up for election in 2022 are those previously decided in 2016, a good year for Republicans. Republicans are defending two seats in states Biden won, while Democrats are not defending any seats in states Trump won.

Major consequences

The outcome of this election will have major consequences. If Republicans take one or both chambers, Biden’s legislative agenda will be doomed. Furthermore, in 2023, the debt ceiling will likely need to be raised again. Republicans in a split or Republican-controlled Congress could use the threat of default or government shutdowns to extract political concessions, either of which would cause unnecessary economic pain and uncertainty (see Economische Opinion 31Januari 2019).

If Democrats maintain control, a shutdown or debt ceiling crisis are less likely. However, keeping a narrow Senate majority will not dramatically improve Biden’s chance of passing elements of his stalled Build-Back-Better bill, a bill originally containing 3.5 trillion USD in new spending on climate change and social policies. The two moderate Democratic senators currently blocking the passage of the bill, Joe Manchin and Kyrsten Sinema, are up for re-election in 2024 and will likely want to shore up their centrist credentials beforehand.

If Democrats maintain control of the House and increase their majority in the Senate to 52 seats or more, however, expect more legislative action. Not only will elements of Build-Back-Better be easier to pass, but Democrats might also aim for abolishing the filibuster rule that requires 60 out of 100 Senate votes to advance most legislation. Without the filibuster to hold them back, Democrats would move forward with legislation on voting rights, immigration, and other legislation that could affect the economy.

Conclusion

The US is up for another nail-biting election. Though Republicans have the upper hand, it is not a done deal for them. Much can change from now till November. What is certain, is that the election will have major impact on what turn the country is taking. Climate change, social policy, immigration, and much more are all on the ballot this November.