French need pension reform but risk seeing little change

Since early December 2019, trade unions in France have organised a series of strikes and protests against the government’s planned pension reform. The reform, which is necessary to improve the sustainability of government finances, also aims to improve the transparency, efficiency and equity of the pension system. So far, the economic impact of the strikes remains contained, but any extension or a broadening of the strikes could impact confidence and GDP growth, like during the gilets jaunes protests. We believe that the chances of Macron succeeding are still relatively high but so is the risk that the reform will be hollowed out by too many exceptions and concessions.

Reform highly needed

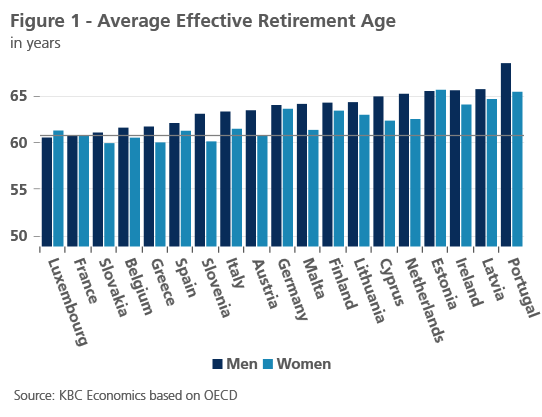

Pension reform is highly needed in France for two main reasons. First, the current system is too costly. This is due to the fact that France has one of the lowest effective retirement ages in the Eurozone. French men especially retire relatively early compared to men in other countries (see figure 1).

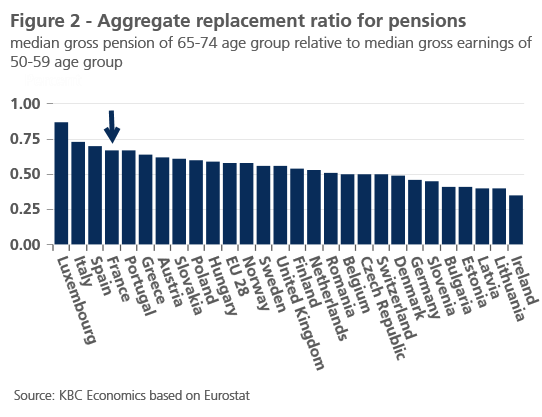

On average, French men and women spend around a third of their life in retirement. In addition, France also has a high replacement rate. This is the ratio between the median gross pension of the 65-74 age group relative to the median gross earnings of the 50-59 age group (see figure 2). This results in a high government spending gap vis-a-vis peer countries. Currently, France spends almost 20 percent more on pensions than peer countries like Italy, Germany, Sweden and the UK (IMF Article IV 2019).

Second, the current pension system is highly fragmented and unfair. It comprises 42 public and private schemes with costly privileges to some specific professions, such as the train drivers. The Macron government wants to replace this with a universal system based on points. Each point would give the same rights, regardless of the sector in which an employee works. This would improve the transparency and intergenerational and intersectoral equity of the pension system.

Raising taxes or social security contributions to fund the current pension system is difficult given France’s already high level of public revenue and expenditure. President Macron’s plan primarily relies on an increase of the effective retirement age, mostly on a voluntary basis, to tackle the budgetary strain of pensions. The ending of generous pension schemes for some groups, in contrast, will largely be counterbalanced by more generous pension schemes for other groups.

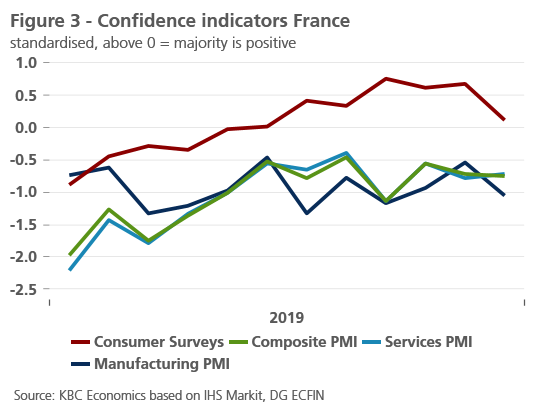

Risk of adding too much water to wine

Chances of President Macron succeeding in reforming the pension system are relatively high. According to an IFOP poll from November 2019, 76% of French people support the overhaul of the pension system and Macron, who has seen no significant change in his approval rating since the onset of the strikes, was elected on the promise to transform the French social model and welfare system. With the 2020 regional elections and the 2022 presidential election coming closer, backing down could mean a loss in votes from his support base. To limit unrest and ease the transition, the plan is to introduce the reform gradually and only in a couple of years. In addition, promises were made that accrued benefits will not be lost.

The road to the reform will, however, be paved with obstacles. President Macron is not the first French politician that has tried to reform the pension system. An earlier attempt by Alain Juppé in 1995 was cancelled after three weeks of strikes which impacted sentiment and economic activity (a temporary decline of -0.2 percentage points of GDP). This time, only consumer sentiment seems to be somewhat affected by the strike (see figure 3). Compared to 1995, the strike seems to have a more limited impact because of the widespread use of teleworking, the breakthrough of e-commerce and the lack of strike participation in the private sector transportation firms (substitute for railway transport). If the strikes continue for a longer period of time or extend in scope, however, sentiment could still start to deteriorate and impact GDP growth. This in turn would put pressure on the government.

The impact of the strikes is not the only obstacle President Macron faces. In spite of the strong support for the pension reform, only 36% of the French people believe that Macron will succeed in pushing through the reform in a fair way. This has resulted in high initial support levels for the protest. Support and strike participation rates started waning more recently, mainly as the strikes caused holiday travel chaos. To ease tensions further, the president has already granted exceptions to police, air stewards, pilots, medical personnel, etc.

Another obstacle and the main point of contention in negotiations between the government and the unions is the retirement age. The government wants to increase the age to qualify for a full pension to 64, beyond the official retirement age of 62. This is a ‘red line’ for most unions. That is why the government temporarily withdrew this measure last weekend in order to make room for negotiations on alternatives to ensure the affordability of pensions.

To conclude, an overhaul of the French pension system is inevitable to keep the pension burden in check and to increase fairness. President Macron has a good chance of getting the reform pushed through. However, there are two big problems arising as the situation stands. First, the exceptions that President Macron has granted so far raise fears that the end-result of the reform will be a pension system with as many exceptions as there are schemes in the current system. Second, if no alternative to raising the retirement age is found, the reform could prove to have a very limited impact on the long-term sustainability of public finances. Hopefully, further concessions by the French government will not lead to an erosion, but only to a limited slowdown in reforms. It is better to go for a good but gradual reform than substituting the existing complex and inefficient pension system with one with the same characteristics.