E-commerce: the last mile counts

E-commerce has been on the rise in Belgium for several years now. As a result, the amount of home deliveries has also increased. From a sustainability perspective, home deliveries are not always the best option. In part because the last miles to the consumer's door are often very polluting. It is therefore important to think about more sustainable alternatives and about raising consumer awareness. Finally, brick-and-mortar shops remains a valuable option for some products.

E-commerce increasingly popular

E-commerce is gaining considerable popularity in Belgium. For some time now, the volume of online orders has been increasing more strongly than purchases in brick and mortar shops. According to The House of Marketing's E-commerce Barometer, Belgian webshops had a combined turnover of 8.2 billion euros and processed a total of 85 million transactions in 2019, an increase of 17% and 22% respectively compared to the previous year. In comparison, e-commerce turnover in the Netherlands only rose by 7% in 2019 (Thuiswinkel Markt Monitor 2019). This difference in growth figures is mainly due to the fact that our northern neighbours have been walking the digital shopping path for a longer time. In absolute figures, the total turnover from e-commerce is therefore much higher in the Netherlands (€26 billion in 2019). But Belgium is catching up.

Preliminary figures for 2020 show that the coronavirus crisis has reinforced the e-commerce trend. Due to the temporary lockdown of brick and mortar shops and infection fears, many new consumers have found their way to online shopping. According to the BeCommerce Market Monitor, spending on products online increased by 33% in the first half of 2020. The number of online purchases of products also peaked during that period at an unprecedented level of 59.1 million. It is likely that the e-commerce figures for products will drop somewhat now that brick and mortar shops are open again. However, it is generally accepted that there will be some lasting impact of the coronavirus crisis on online sales of goods. The figures for online sales of services were less positive in the first half of the year, but this was mainly due to the sharp decline in ticket sales for attractions and events and travel sales.

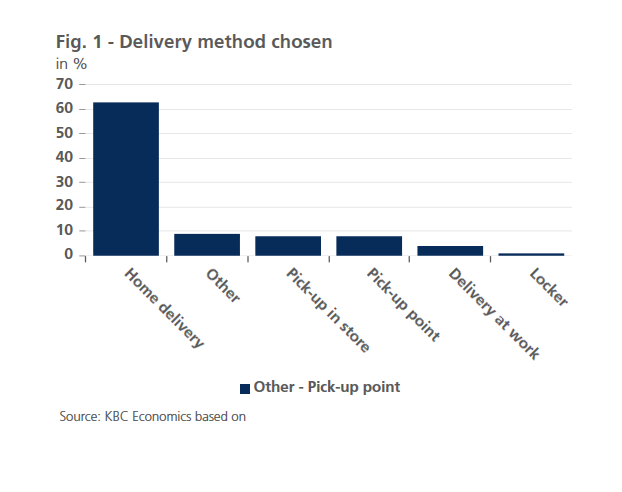

The consequences of the increasing popularity of e-commerce are also noticeable on the streets. Delivery vans have been omnipresent on the roads in recent months. Indeed, some 63% of all e-commerce orders are delivered at home, according to the Comeos E-Commerce report of 2019 (see figure 1).

Last mile = expensive mile

The growth boost to e-commerce in coronavirus times deserves attention from an environmental point of view. The last miles of the delivery route are not only the most expensive but often also the most polluting. In the urban context, factors such as congestion, noise and air pollution play a greater role, while in the rural context, long distances are the main problem.

One could argue that the last mile has to be driven anyway, either by the transport company or by the consumer who picks up the package at a distribution point. Nevertheless, there are reasons why home deliveries score more poorly in terms of sustainability. First and foremost, there are the failed delivery attempts. In these cases, the same last miles have to be driven several times.

In addition, most courier companies use relatively polluting delivery vans for the whole journey, including the last miles. If central distribution points are used, e.g. collection in shops or post offices, the last miles are more often covered in a less polluting way, e.g. by bicycle or on foot. The Transportation Behaviour Survey 2018-2019 of the Institute for Mobility shows that about half of journeys of less than 5 kilometers (3.11 miles) to shops in Flanders, are travelled on foot or by bicycle. Moreover, the consumer can often combine the pick-up, by any means of transport, with another activity, especially when the distribution points are located near supermarkets or other busy places.

Alternatives worth considering

There are more and more exceptions to the rule that courier companies cover the entire distance with more polluting means of transport. Experiments are being carried out in towns and cities with e-bike deliveries and progress in the field of electric cars means that a more environmentally friendly way of delivery is also becoming available outside of city centers. In the future, large-scale deliveries via drones and 3D printing options may be added to this. We are not there yet, but luckily consumers already have some options to shop a little more sustainably.

As already mentioned, consumers can often choose for delivery at a distribution point nearby or at work. Scenario analyses carried out by KU Leuven's computer science department in 2016 showed that if 75% of deliveries were made via collection points, the cost and footprint of 'the last mile' would be reduced by 60 to 80%. Crucial elements to convince consumers to choose this option are the density of the network of collection points and their opening hours. In addition, the delivery process at distribution points could be further optimised by moving away from fast delivery options such as same-day or next-day deliveries wherever possible.

Online shops can also play their part in persuading consumers to go for more sustainable delivery options. Delivery prices are often the same for home delivery and pick-up. If home delivery were to be made more expensive than the alternative delivery options, this could reduce the proportion of home deliveries as e-shoppers are typically price sensitive. Efforts to raise awareness could also be made by vendors, for example by indicating the CO2 impact of different delivery options.

Brick and mortar shopping also has its advantages

Finally, there is the problem of frequent returns of ordered items in e-commerce. If the consumer continues to place and return orders until the purchased item meets the requirements, or if he/she returns goods frequently and in large quantities, the environmental impact of e-commerce increases. In these cases, shopping in brick and mortar shops can be a better solution from a sustainability point of view. After all, in brick and mortar shops, purchases such as garments can be tried on immediately, thus avoiding returns. In addition, consumers can view or try on as many items as they like within one shop without the need for extra travel.

It is true that the consumer often has to travel some miles to get to shops, but shops are usually located in clusters (shopping streets, shopping centres,...) so that the consumer can often compare products between shops in one go and combine several purchases. In many cases, the distance to the shop can also be covered in a sustainable way, such as on foot, by bicycle or by public transport. An additional advantage: brick and mortar shops have had a very hard time in recent months and will welcome consumers with open arms (and mouth masks).